X

Research source

Knowing how to account for negative goodwill is an important part of accounting for acquisitions.

Determining Fair Value

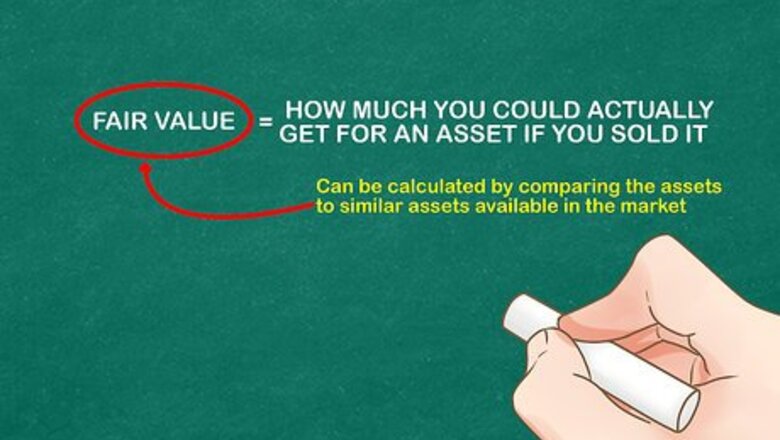

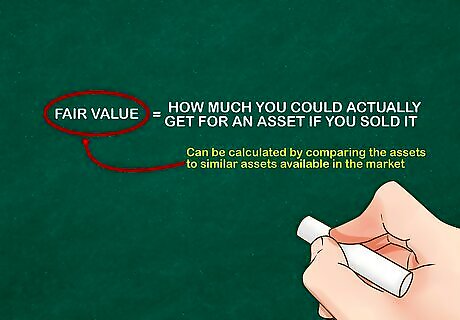

Understand how fair value is found. Fair value represents the price that could be gained from the sale of an asset or the amount paid to transfer a liability at the present date in the open market. Essentially, fair value represents how much you could actually get for an asset if you sold it. This distinguishes it from book value, which is based on depreciation and other calculations. Fair value can be calculated by comparing the assets to similar assets available in the market. For more on determining fair value, see how to calculate asset market value.

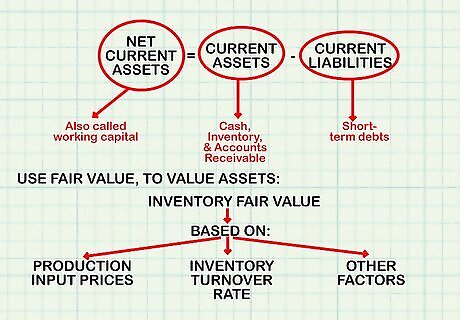

Calculate fair value for net current assets. Net current assets represents the value of all current assets (like cash, inventory, and accounts receivable) minus all current liabilities (short-term debts). This is also called working capital. Use the fair value principle explained above to value these assets. Inventory fair value may be more or less than book value. This depends on numerous factors, from production input prices to inventory turnover rate. A low inventory fair value is common in bargain purchases.

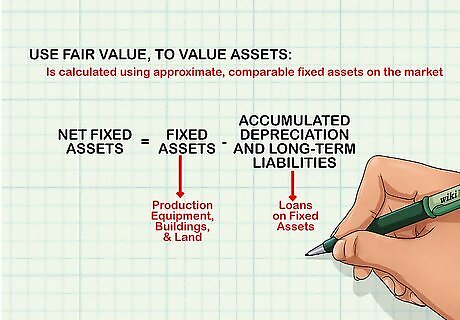

Find fair value for net fixed assets. Net fixed assets are calculated as the value of the company's fixed assets (production equipment, buildings, land) minus accumulated depreciation and long-term liabilities (loans on fixed assets). This also includes any improvements made to fixed assets. Again, fair value may be calculated using approximate, comparable fixed assets on the market.

Estimate fair value for identifiable intangible assets. In addition to tangible assets, some intangible assets are identified and valued during the purchase process. These include items of a contractual or legal nature, like patents or customer relationships, and are also valued using fair value principles. These, however, are much harder to value than tangible assets. The valuation of these assets is best left to experienced accountants and valuation specialists. These intangible assets can include: Unique technologies Brand names Licenses Workforce ability Agreements with customers or competitors Usage rights (such as EM spectrum rights)

Calculating Negative Goodwill

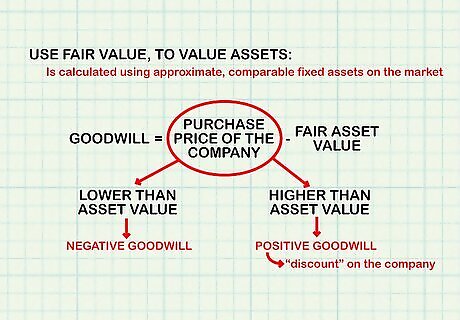

Know how goodwill is calculated. Goodwill is simply the difference between the purchase price of the company and the fair value of its assets, both tangible and intangible. When the purchase price is higher than the asset value, there is positive goodwill; when it is lower, there is negative goodwill. Negative goodwill represents a "discount" on the company.

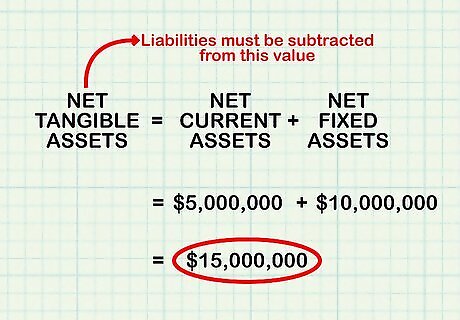

Sum up net tangible assets. Add up the net fair value of all of the company's tangible assets, including current and fixed assets. Remember that any liabilities present must be subtracted from this value. For example, imagine that the company has $5 million in net current assets and $10 million in net fixed assets. Add these two together to get a total of $15 million.

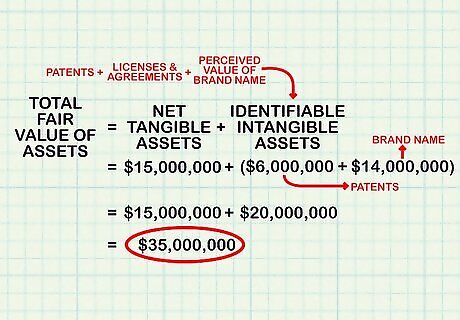

Add identifiable intangible assets. Total up the fair value of any intangible assets identified in the purchase process. These include the value of any patents, licenses, and agreements, as well as the perceived value of the company's brand name. Add this value to net tangible assets to get the total fair value of the company's assets. For example, if the assessed value of the same company's intangible assets comes to $20 million, including $6 million in patents and $14 million in the brand name, add this figure to total tangible asset value to get $35 million ($15 million + $20 million) in total asset value.

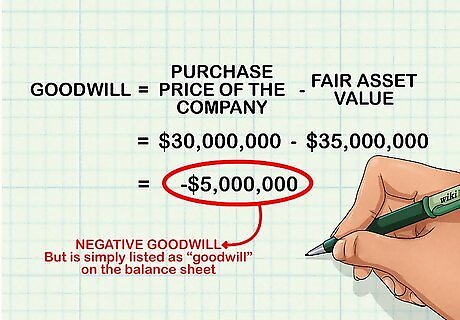

Subtract total asset value from the purchase price. Take the total fair value of the company's assets found in the last step and subtract it from the purchase price of the company. The result, assuming the purchase price was lower than the asset value, will be negative goodwill. If the purchase price for the same company is $30 million, subtract the value of the company's assets, $35 million, from this number to get goodwill. So, the negative goodwill in this case is $30 million - $35 million, or $-5 million. Even when the goodwill is negative, it is still listed simply as "goodwill" on the balance sheet. It is listed as negative number though.

Making Accounting Entries

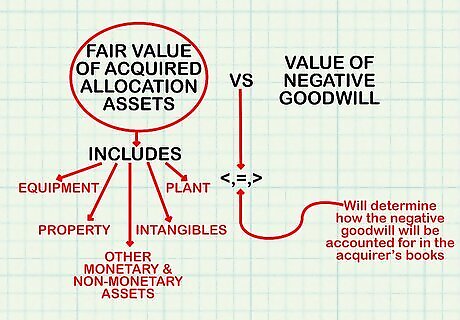

Compare the fair value of acquired allocation assets to the value of negative goodwill. Allocation assets are broadly defined as non-current assets obtained by the purchaser in an acquisition. These include plant, property, equipment, intangibles, and other non-current and non-monetary assets. Total the fair market values of these assets and compare it to your calculated negative goodwill value. Whether negative goodwill is more than, equal to, or less than the allocated asset value will determine how the negative goodwill will be accounted for in the acquirer's books.

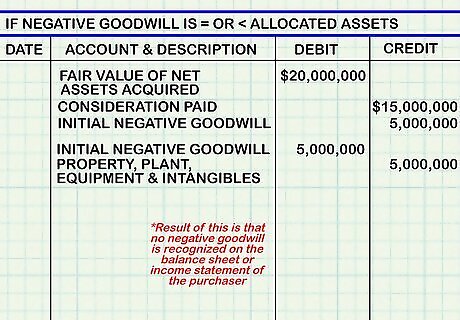

Record a reduction in allocation asset value. If the negative goodwill value is equal to or less than the value of allocated assets, the allocated asset value is reduced by the complete amount of the negative goodwill. The transaction is recorded as first as a debit to fair value of assets acquired for the value of net assets acquired plus the negative goodwill value, a credit to total consideration paid for the cost of acquiring the company, and a credit to initial negative goodwill for the value of the negative goodwill. Then, an entry is made to adjust the allocation assets by debiting initial negative goodwill for the full amount of negative goodwill and crediting allocation assets (or property, plants, equipments, and intangible assets) for the same value. For example, imagine that a company whose net assets are valued at $20 million is acquired for $15 million. The negative goodwill here is $5 million. The value of allocation assets is calculated at $6 million. First, debit fair value of net assets acquired for $20 million, credit consideration paid for $15 million, and credit initial negative goodwill for $5 million. Then, debit initial negative goodwill for $5 million and property, plant, equipment, and intangibles for $5 million. The result of this is that no negative goodwill is recognized on the balance sheet or income statement of the purchaser.

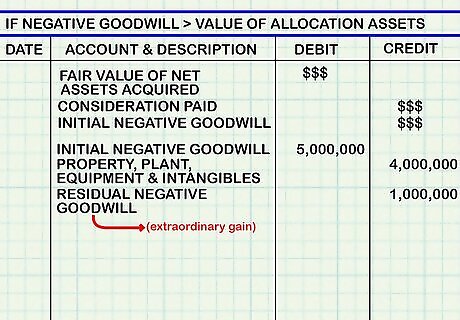

Calculate residual negative goodwill. If the value of the negative goodwill is larger than the value of allocation assets, the purchaser will have to reduce the allocation asset value to zero and then recognize the value of the residual negative goodwill. The accounting entries for this situation are similar to those in the first case, with one exception. The initial negative goodwill is still reduced by its full value, but the property, plant, equipment, and intangibles account is reduced by its full value, with the leftover being credited to residual negative goodwill (extraordinary gain). Imagine that in the previous example, the value of the allocation assets was instead $4 million. You would still perform the first set of entries (net assets acquired, initial negative goodwill, and consideration paid) in the same way, but in the second, you would debit initial goodwill for $5 million, credit plant, property, equipment, and intangibles for $4 million, and credit residual negative goodwill (extraordinary gain) for the difference, $1 million.

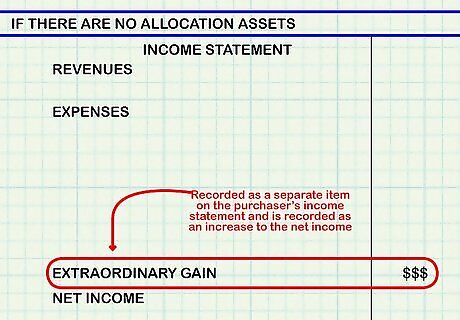

Recognize residual negative goodwill. If there are no allocation assets, you should record all of the negative goodwill as an extraordinary gain. In this case, there is no need to allocate an initial negative goodwill amount. For this case or for the case of residual negative goodwill, the extraordinary gain should be reported as a separate item on the purchaser's income statement. The extraordinary gain should be recorded as an increase to net income.

Handling a Bargain Acquisition

Look for bargain purchase warning signs. Any transaction that results in negative goodwill should have a reason behind that result. That is, companies aren't sold for a discount unless they have fallen on hard times. Be sure to assess whether or not this is the case if your calculations for goodwill give you a negative number. If not, your assessments for fair value may have been too high. In general, companies sold for a discount show one or more of the following signs: Recent financial hardship Lack of potential buyers The business was sold quickly The seller was forced to sell Uninformed seller (about market trends, growth projects, etc.)

Identify that there will be negative goodwill. If you are appraising a company for sale, ask the seller if they expect that the company will be sold at a discount. Having the knowledge that a company will likely be sold at a discount can make other decisions, like certain aspects of determining fair market value, much easier during the appraisal process. Again, make sure that there is an accompanying reason that the company is being sold this way.

Communicate with all parties. If you determine that negative goodwill is likely, inform both the buyer and seller immediately. You should also contact any other appraisers or auditors working on the deal so that the valuation can run smoothly.

Evaluate differences in the rates of return. The calculated internal rate of return (IRR) and weighted average cost of capital (WACC) are often misaligned in a bargain purchase. Most of this has to do with the fact that the IRR is calculated using the purchase price, while the WACC is not. These differences can result in different valuations for the company and its assets. Identify why these rates are different and assess whether or not you can justify why this is so. In some cases, a separate valuation of the company may be necessary.

Comments

0 comment