Researching 529 Plans

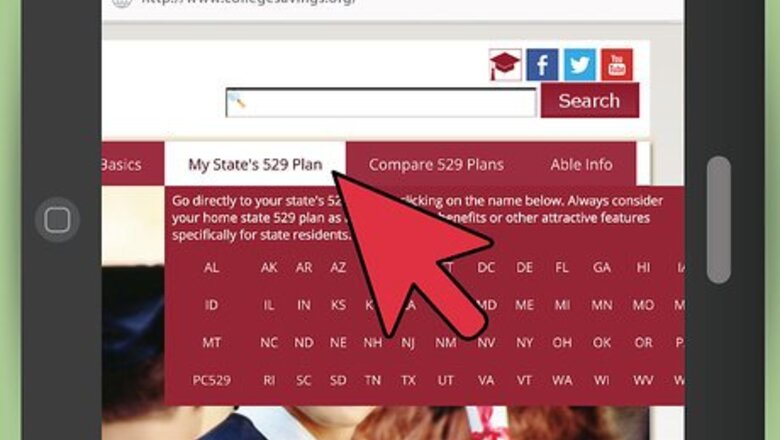

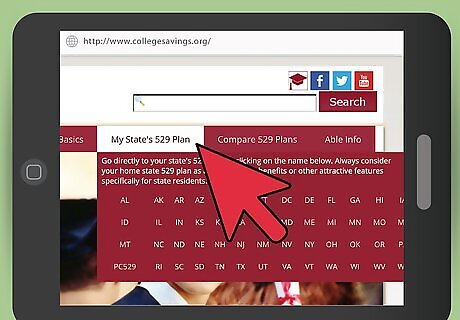

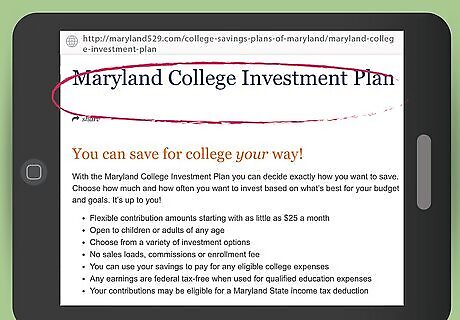

Check your state’s plan. Many states offer a state-sponsored 529 plan for college investment. Each state determines the structure and options that go along with its own plan. Some states offer matching grants and other benefits to in-state residents who buy into the state-sponsored 529 plan. Some of the benefits of investing in your own state’s sponsored 529 plan are: state tax deductions matching grants scholarship opportunities protection from creditors exemption from state financial aid calculations

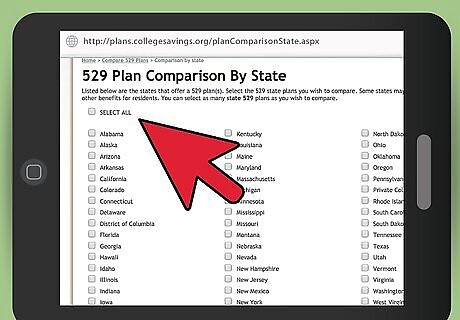

Consider plans from other states. If you look at plans from states other than the one where you reside, you may find that another state offers a plan with strong benefits and does not have an in-state residence requirement. You might not benefit from all the options that are available to an in-state resident, but you may find that other benefits are still strong enough to make it a good choice. The College Savings Plans Network, CSPN.org, has a search feature that makes it easy to compare plans from multiple states.

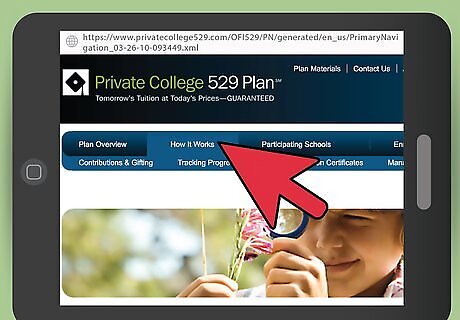

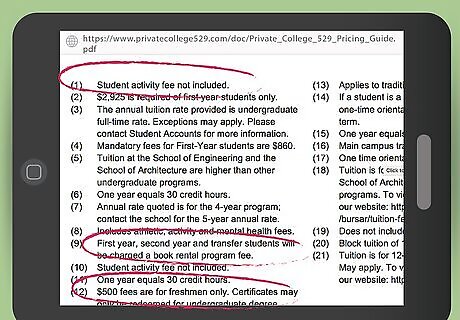

Investigate privately sponsored 529 plans. The Private College 529 Plan is a prepaid tuition plan that is owned and sponsored through a consortium of over 270 private colleges and universities around the country. A private plan will not provide the tax benefits that many state-sponsored plans provide. However, it is still an excellent way to save for college and secure your investment over time. By locking in the college credits now, you are guaranteed to have the payments for college in the future.

Choosing the Type of Plan you Want

Consider a prepaid tuition plan for more security. A prepaid tuition plan allows you to lock in tuition rates at today’s prices, at eligible public and private universities. Most prepaid tuition plans are sponsored by the state government and have some residence requirements. These plans generally have a limited enrollment period. Your investment in a prepaid tuition plan is guaranteed by your state, in most cases. With a prepaid tuition plan, you generally purchase “credits” or “units” at today’s rates. When your child attends college, the plan will pay for the number of credits purchased, at the future tuition rate. So while your money does not exactly earn interest in the traditional sense, you can determine the growth by comparing tuition costs over time. Selecting a state-sponsored plan does not lock you in to a state college or university. With most plans, the money that you invest can be used for tuition and fees and any college or university, public or private.

Be aware of the fees for a prepaid tuition plan. These fees will generally be enrollment fees and administrative management fees. The fees will vary from state to state, so ask before you invest.

Choose a college investment plan for additional flexibility. With a college savings plan, you invest in a choice of investment options, such as stock mutual funds, bond mutual funds and money market accounts. The money is invested and managed by a broker. Investments are more flexible than most prepaid tuition plans, but the money is not guaranteed by the state. Your investments are subject to fluctuations in the market and may even decrease in value.

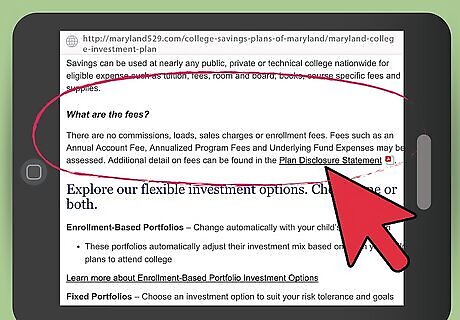

Be aware of the fees for a college investment plan. This type of plan is likely to have enrollment fees, annual maintenance fees, and, depending on the broker who is selling or investing the account, a range of additional broker’s fees. The fees will vary depending on the broker and the investments that you select. Ask questions about fees and get informed before you invest your money. You may be able to reduce your broker’s fees if you invest a large enough amount of money and maintain the stated minimum balance. Ask the broker about these “break-point discounts” if you are interested.

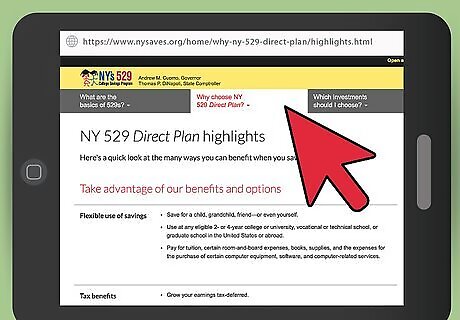

Look for “Direct Sold College Savings Plans” to avoid paying some fees. In some states, you can buy directly into a college savings plan without paying some of the fees associated with other plans. If a plan is labeled as “Direct Sold,” then you are buying directly into the plan, without the use of an adviser or broker, and thus can avoid some fees.

Comments

0 comment